What’s the newest information from the financial savings market? We monitor all the newest strikes and maintain you up to date recurrently with the important thing developments.

Acquired a financial savings story to share? Electronic mail: amichael@forbesadvisor.com

19 October: Savers Urged To Be Proactive As Inflation And Returns Rise

The highest price for simple entry financial savings accounts has greater than doubled since final yr, however with inflation stubbornly excessive, savers should be proactive find the most effective offers, writes Bethany Garner.

Though rising rates of interest are welcome information for savers, inflation — which hit 10.1% in the 12 months to September in accordance with figures right this moment from the Workplace for Nationwide Statistics — continues to erode the worth of money.

Rachel Springall at Moneyfacts, mentioned: “It’s crucial savers don’t change into apathetic to change at a time when competitors within the prime price tables is rife.

“Top fixed rate bonds are reaching heights not seen for a few years as challenger banks compete to entice financial savings deposits. However this has additionally seen offers change inside a short while body, so swift motion is sensible to seize a prime price financial savings deal.”

The highest price for simple entry accounts at present pays 2.55% AER, whereas the best price savers may entry a yr in the past was simply 0.65% AER, in accordance with Moneyfacts. Curiosity on the highest one-year fastened price bond is up 1.89% in contrast with October final yr.

The most recent supplier to spice up its charges right this moment was Nationwide. The constructing society is upping returns throughout a spread of financial savings accounts by as much as 1.20% for present prospects from 1 November.

Private Financial savings Allowance

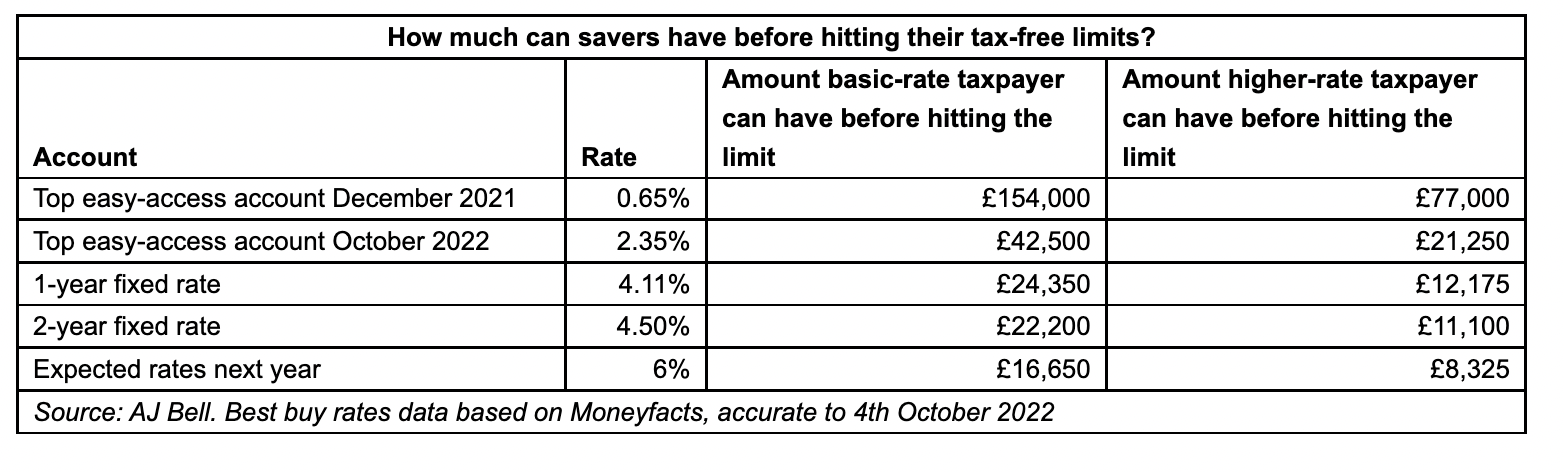

However greater financial savings charges are additionally pushing extra savers past their Personal Savings Allowance – the edge at which tax begins to be charged on curiosity earned.

Figures from investmenr platform AJ Bell present that, in December 2021 when Financial institution price stood at 0.1%, primary price taxpayers – who can earn £1,000 of curiosity tax-free a yr – may maintain £154,000 in a prime easy accessibility account earlier than paying tax. As of 4 October 2022, this steadiness had dropped to only £42,500.

Greater price taxpayers – who can earn £500 of curiosity tax-free a yr – may maintain as much as £77,000 in a top-paying financial savings account, which in comparison with £21,250 on 4 October.

If the Financial institution of England continues to hike rates of interest, extra savers will probably be hit with tax on their curiosity — many for the primary time.

Laura Suter, head of private finance at AJ Bell, mentioned: “If the Base price hits the 6% it’s anticipated to subsequent yr and easy accessibility financial savings charges matched that, a basic-rate taxpayer may solely have £16,650 of their account earlier than they hit the restrict — and for a higher-rate taxpayer this may drop to £8,300.”

To keep away from paying tax on their curiosity, Ms Suter expects savers will flip to ISAs – a financial savings ‘wrapper’ during which people can save as much as £20,000 every tax-free.

Nevertheless, since ISAs usually pay decrease rates of interest, savers could also be confronted with the selection between greater charges or a decrease tax invoice.

13 October: First Direct To Double Money ISA Charge

First Direct is doubling the rate of interest on its money ISA from 0.70% to 1.40% AER (variable) on 20 October, writes Bethany Garner.

The mobile-first financial institution can be elevating charges throughout three different financial savings merchandise. Its easy accessibility Financial savings Account can pay 0.50% AER (variable) from 20 October — up from 0.40%.

Its Bonus Financial savings Account can pay as much as 1.65% AER on balances beneath £25,000, and 0.75% AER on balances above £25,000. The account rewards savers for not accessing their money. In the event that they make a withdrawal, the brand new price drops to 0.50% AER for that calendar month.

From the later date of 28 October, First Direct’s one-year Fastened Charge Saver will rise by a full share level, from 1.25% to 2.25% AER.

First Direct is the newest of a number of suppliers to extend charges on its financial savings accounts in response to consecutive Financial institution price hikes.

Whereas information of will increase is welcome, stubbornly excessive inflation continues to be eroding any actual returns on savers’ money. With annual inflation working at 9.9%, the onus is on savers to check offers and discover the highest-paying account for the entry required to their money.

5 October: Barclays Wet Day Saver Pays Up To five.12% AER

Barclays has launched a linked financial savings account paying a prime price of 5.12% AER (variable), writes Bethany Garner.

The financial institution’s new Wet Day Saver is an easy access account which permits eligible savers to make limitless deposits and withdrawals – and might be opened with simply £1.

At 5.12% AER, the returns on the account are greater than double these supplied by main open-to-all easy accessibility financial savings accounts.

Nevertheless, solely Barclays present account holders who’re signed as much as the Blue Rewards scheme are eligible. Blue Rewards fees a month-to-month price of £5 however, offering your Barclays present account is credited with no less than £800 a month and has no less than two outgoing direct debits arrange, this price is repaid into your Rewards Pockets. This may be accessed and managed on-line or on the Barclays app.

The highest price of 5.12% AER solely applies to balances of as much as £5,000. Any balances above this threshold earns a a lot decrease 0.15% AER (variable).

You may maintain as much as £10 million within the Wet Day Saver however savers with greater than £5,000 who don’t want entry to their money will discover greater returns from a fixed rate savings account.

For instance, £10,000 deposited in a set price bond paying 4.50% AER would earn £450 in 12 months. The identical deposit left untouched in Barclays’ Wet Day Saver for 12 months would earn £263 of curiosity.

5 October: Headline Charge Hits 4.75%

Nationwide Constructing Society is launching three fastened price on-line bonds and elevating rates of interest for a number of different accounts, writes Bethany Garner.

The UK’s largest constructing society is now providing:

- one-year fastened price bond paying 4.00% AER

- two-year fastened price bond paying 4.50% AER

- three-year fastened price bond paying 4.75% AER.

Every account might be opened and managed completely on-line or by Nationwide’s cellular banking app. The minimal opening deposit is £1.

In the meantime, the curiosity paid on Nationwide’s present fastened price accounts is about to rise by 0.50%:

- one-year fastened price bond will now pay 3.25% AER

- two-year fastened price bond will now pay 3.50% AER.

Nationwide has additionally introduced it would improve charges on its triple entry financial savings accounts.

The One Yr Triple Entry On-line Saver can pay 2.10% AER — up from 1.75% — and the One Yr Triple Entry On-line ISA will now pay 2.00% AER, up from 1.50%.

These accounts permit as much as three withdrawals all through their 12-month time period. If any extra withdrawals are made, the rate of interest drops to 0.30% AER.

Nationwide’s Flex Immediate Saver account, which permits limitless deposits and withdrawals, will see charges doubled from 1.00% to 2.00% AER over the following 12 months. This account is offered to Nationwide present account holders solely.

The society is providing a £200 switching incentive to those that change to its present accounts from different banking suppliers.

Tim Riley, director of banking and financial savings at Nationwide, mentioned: “We perceive there are many savers who’re glad to lock their cash away for a time frame, which is why we will probably be providing extremely aggressive charges on our bonds.”

29 September: Household Constructing Society Gives Premium On Financial institution Charge

The Household Constructing Society has launched a Two Yr Tracker Charge Bond — a financial savings account with a variable rate of interest that strikes consistent with the Financial institution of England Financial institution price.

At the moment at 2.60% AER (gross), the account’s rate of interest is about at 0.85% above the present Financial institution price. It modifications to trace the Financial institution price because it stands on the primary day of every month.

The Bank rate rose from 1.75% to 2.25% in September, so the bond can pay 3.10% AER from 1 October.

To open the account, savers should deposit no less than £5,000. As soon as 15 days have elapsed, no extra deposits might be made. Withdrawals usually are not permitted till the account matures two years after opening.

It’s value nothing that some fixed-rate savings accounts are at present paying greater charges. For example, the 2-Yr Fastened Time period Deposit from Investec provides an AER of 4.25% (gross) on balances from £1,000.

Nevertheless, if the financial institution price continues to rise – it has risen seven instances since December 2021 – the Household bond may outpace these top-paying accounts.

With annual inflation at 9.9% eroding the worth of financial savings, an account that passes on financial institution price rises to shoppers with out requiring them to buy round could possibly be useful.

If the financial institution price goes down, although, savers locked into this two-year fastened time period account may miss out on higher returns elsewhere.

27 September: NS&I Provides £76 Million To Premium Bonds Prize Fund

Nationwide Financial savings and Funding (NS&I), the Authorities-backed financial savings financial institution that oversees Premium Bonds, is elevating its prize fund from 1.40% to 2.20% from 1 October 2022.

The change will add round £76 million to the Premium Bonds prize fund, creating 97,752 new prizes within the month-to-month draw.

Most of those will probably be money sums of £50 or £100, however the variety of bigger prizes can be rising. From October, the variety of £100,000 prizes will improve from 10 to 18, whereas the variety of £50,000 prizes will rise from 20 to 35.

There’ll proceed to be simply two £1 million prizes every month.

General, the percentages of every Premium Bond being a winner will enhance from 24,500 to 1, to 24,000 to 1.

Ian Ackerley, chief government of NS&I, mentioned: “That is the second improve to the Premium Bonds prize fund price that now we have made in lower than six months.

“These modifications have helped us make sure that Premium Bonds stay engaging, whereas additionally guaranteeing that we proceed to steadiness the pursuits of savers, taxpayers and the broader monetary companies sector.”

Premium bonds are held by over 21 million individuals within the UK. As a substitute of incomes curiosity, bond holders are entered right into a month-to-month prize draw for tax-free money sums, which vary in worth from £25 to £1 million.

Every £1 invested in Premium Bonds equates to at least one entry into the prize draw, however the minimal funding degree is £25. Savers can select to money out all or a portion of their bonds at any time.

Though profitable a big money prize might assist some savers beat inflation, they might equally win nothing.

Laura Suter, head of private finance at AJ Bell, mentioned: “Savers shouldn’t cling to the ‘projected prize fund determine’ as many Premium Bonds holders get zero return on their financial savings.“Most savers can be higher off with a typical easy-access savings account that pays out a assured price of curiosity.”

26 September: Over 11 Million Brits Have Much less Than £100 In Emergency Funds As UK Financial savings Week Will get Underway

An estimated 11.5 million UK adults have lower than £100 in emergency financial savings, in accordance with analysis by the Constructing Societies Affiliation (BSA) – the organisation behind the inaugural UK Financial savings Week which begins right this moment.

The marketing campaign goals to lift consciousness of the significance of saving habits, and supply steering to shoppers on reaching their saving targets.

Andrew Gall, head of financial savings and economics at BSA, mentioned: “Whereas the midst of a cost-of-living crisis may look like an odd time to launch actions encouraging good financial savings habits, those that are in a position to save can profit from constructing their resilience to future shocks.”

The BSA’s analysis, which surveyed 2,000 UK adults in August 2022, revealed {that a} rising variety of shoppers are dipping into financial savings to fulfill on a regular basis bills.

In keeping with the survey, 36% of shoppers are turning to financial savings to fulfill the mounting price of necessities. An additional 55% of savers say they’re setting apart much less resulting from cost-of-living pressures, whereas 35% have stopped saving altogether and 13% haven’t any financial savings in any respect.

Nevertheless, the analysis additionally discovered that 64% of respondents, who at present haven’t any financial savings, say they might be capable of put aside £10 a month.

A good portion of shoppers will not be getting the most effective returns, nevertheless. Nearly 1 / 4 (23%) of savers don’t examine rates of interest earlier than opening an account, whereas a 3rd (33%) examine charges however don’t examine them with different accounts.

Whereas some financial savings suppliers have begun passing on the good thing about the newest interest rate rise to savers within the type of extra aggressive savings accounts, many have but to take action.

And with annual inflation working at 9.9%, successfully eroding the worth of money extra rapidly, the onus is on savers to check offers and discover the highest-paying account for the entry required to their money.

22 September: Returns Inch Greater However Financial savings Nonetheless Battered By Inflation

Savers had been handed optimistic information right this moment when the Financial institution of England’s rate-setting Financial Coverage Committee (MPC) raised rates of interest for the seventh time in a row. At 2.25% the Financial institution price is now at its highest degree in 14 years.

Yorkshire Constructing Society was fast off the mark following the announcement. Inside minutes of the information, it confirmed it would increase rates of interest on all its variable price financial savings accounts – however by 0.30 share factors in comparison with the 0.50 share level improve within the Financial institution price.

The society’s easy accessibility Web Saver Plus Difficulty 12 can pay 1.80% AER from October. The speed on its Loyalty Common Saver Difficulty 2 will rise to five.3% AER.

The charges will probably be utilized to accounts routinely on 5 October. Different banks and constructing societies are anticipated to go on rises to prospects within the coming days.

Marcus by Goldman Sachs has additionally introduced it will likely be elevating charges on each its variable price accounts — the On-line Financial savings Account and Money ISA – by 0.30%.

Each accounts are at present paying 1.80% AER, which features a 12-month bonus price of 0.25%. Bear in mind this bonus price will drop off on the anniversary of opening the account, so it might be value checking whether or not higher choices can be found after the primary yr.

Whereas information of will increase is welcome, stubbornly excessive inflation continues to be eroding any actual returns on savers’ money. Inflation, as measured by the Client Costs Index (CPI), hit 9.9% within the 12 months to August – which was over 14 instances greater than the common easy accessibility financial savings price over the identical interval, in accordance with analysis from funding platform interactive investor.

Any delay between the newest hike and improve in financial savings charges will additional widen the hole between inflation and returns.

Becky O’Connor, head of pensions and financial savings at interactive investor, mentioned if the rise within the Financial institution price is handed on to savers and has the impact of bringing down inflation, money financial savings may, as soon as once more, begin to look engaging: “This could possibly be particularly welcomed by older individuals, who usually have extra constructed up in financial savings, and in addition usually want the decrease danger of money in comparison with the inventory marketplace for their life financial savings.

“Individuals with financial savings have had years of low returns and this newest price rise, which is important, may actually flip the tables again of their favour.”

21 September: Aggressive Gives Immediate Enhance In Assured Charges

Savers are turning to fixed-term financial savings accounts to lock in more and more aggressive charges.

Funding platform Hargreaves Lansdown reported a 40% uptick within the variety of new fixed-term deposits it has acquired over the past 12 months.

Fastened-term financial savings accounts supply assured rates of interest for a set interval in change for forfeiting entry to your money.

Tom Higham, performing head of financial savings at Hargreaves Lansdown, mentioned: “We’re seeing significantly extra purchasers utilizing fastened time period deposits over easy accessibility. As much as 80% of all new flows are heading into fastened time period deposits, up from round 50% a yr in the past.

“Persons are cashing on fastened phrases as a result of the charges are greater than they’ve been for a decade or extra.”

At 1.75%, the Financial institution of England Financial institution Charge at present stands at a 14-year excessive. Financial institution price is predicted to rise additional tomorrow (September 22) when members of decision-making Financial Coverage (MPC) maintain their subsequent assembly.

Mr Higham expects banks and constructing societies to proceed passing on will increase in Financial institution price to financial savings accounts.

Nevertheless, he added that savers are solely trying to repair of their money for a most interval of two years as they’re anticipating rates of interest to proceed to rise till inflation starts to fall.

25 August: NS&I Pays 3% AER On Newest Inexperienced Bond Difficulty

Nationwide Financial savings & Investments, the federal government backed financial savings establishment, has launched the third situation of its Inexperienced Financial savings Bond, which can pay curiosity at 3% a yr for a three-year fastened time period.

Greater charges can be found for this size of repair – JN Financial institution is paying 3.45%, for instance – however the NS&I bond ensures that deposits will probably be used to assist finance inexperienced initiatives as a part of the UK Authorities Inexperienced Financing Framework.

This can embrace tasks to sort out local weather change, enhance sustainability and improve renewable power capability.

Curiosity at 3% AER over three years on a £10,000 deposit would yield a revenue of round £930. Deposits are permitted within the vary £1,000 to £100,000 however it is very important keep in mind that the cash can’t be accessed in the course of the time period.

Clients must be 16 or over to buy the Bonds from NS&I.

The brand new price compares to the 1.30% paid on the second tranche of Inexperienced bonds issued in February.

NS&I introduced elevated charges throughout its fleet of financial savings merchandise in July after rising the Premium Bonds prize fund in June.

The organisation contributed £1.3 billion to authorities coffers within the first quarter of the monetary yr 2022/23. All financial savings and investments lodged with NS&I profit from a 100% authorities assure.

Its merchandise not often have market-beating charges in order to not unfairly disrupt competitors within the industrial market.

24 August: One-In-Three Adults Have No Entry To ‘Wet Day’ Money

Greater than half of UK adults are set to make use of cash put apart for an emergency due to the worsening cost-of-living crisis, writes Andrew Michael.

Analysis from wealth supervisor Charles Stanley reveals that just about three-quarters of grownup Brits (71%) have a ‘wet day’ fund that may final the common saver simply shy of 5 months.

However as a result of difficult financial local weather, greater than half of respondents (54%) advised the corporate they’re frightened about utilizing up their emergency financial savings, leaving them unprepared for any future monetary crises.

Charles Stanley discovered the common emergency fund would final its proprietor 4 months and three weeks. Simply over 1 / 4 of individuals (28%) mentioned their reserves would cowl them for between two weeks and two months, whereas 10% mentioned they might run out of cash after a fortnight.

Of these with emergency financial savings, 1 / 4 (25%) of respondents mentioned they’ve by no means wanted it, whereas slightly below one-in-10 (9%) mentioned they dip into it lower than yearly.

One-in-eight individuals (12%) mentioned they’ve by no means additional topped up their reserves, though greater than a 3rd (36%) claimed they added month-to-month quantities to their financial savings. One-in-10 (10%) of respondents mentioned they topped up their emergency stash on a weekly foundation.

Charles Stanley mentioned almost one-in-three people (29%) should not have a reserve fund. Almost two-fifths of staff (38%) incomes lower than £20,000 a yr mentioned they don’t have a reserve fund. This proportion fell to only over 1 / 4 (28%) of staff paid between £20,000 and £30,000 and diminished additional for these incomes commensurately greater quantities.

A couple of quarter of staff in employment mentioned they didn’t have an emergency fund, whereas this determine rose to 46% of the job-seeking unemployed.

Lisa Caplan, director of OneStep Monetary Planning at Charles Stanley, mentioned: “Saving right into a wet day pot isn’t at all times individuals’s first precedence, however those that have managed to arrange will be pleased about it in the course of the cost-of-living disaster.

“As ever although, we’re seeing widespread themes after we take a look at who slips by the web. The image is much less optimistic for ladies, low-earners, and people in search of work.”

23 August: Constructing Society Passes On Newest 0.5% Charge Hike

Nationwide Constructing Society has introduced it would increase rates of interest on all variable price financial savings accounts from 1 September 2022.

These accounts are seeing rates of interest rise by 0.50%, consistent with the newest bank rate increase:

- Flex Common Saver price rises to three.00% AER

- Begin to Save 2 price rises to three.00% AER

- Future Saver price rises to 2.00% AER

- Junior ISA price rises to 2.00% AER

- Little one Belief Fund price rises to 2.00% AER

- Sensible Restricted Entry price rises to 1.50% AER

- Flex Immediate Saver price rises to 1.00% AER

The 1 Yr Triple Entry On-line Saver will supply a brand new price of 1.75% AER for the following 12 months, whereas the 1 Yr Triple Entry On-line ISA price is about to rise to 1.50% AER.

Nationwide’s Flex Saver and Flex ISA accounts will see the most important improve of 0.55%, taking charges to both 0.65%, 0.70%, or 0.75% AER relying on the account steadiness.

The Assist to Purchase ISA will bear a barely extra modest price improve of 0.40% to 1.75% AER. The Loyalty Saver, Loyalty ISA and Loyalty Single Entry ISA accounts will see charges rise by 0.35% to 1.60% AER.

Charges on Nationwide’s easy accessibility accounts — the Immediate Entry Saver, Immediate ISA Saver and Cashbuilder — are set to rise by 0.15% to both 0.25%, 0.30% or 0.35% AER relying on the account steadiness.

Tom Riley, director of banking and financial savings at Nationwide, mentioned: “As a mutual we’re at all times eager to assist savers and pay the most effective charges we will sustainably afford, which is why we’re rising charges on all variable price accounts, significantly common savers, loyalty and youngsters’s accounts in addition to our common Triple Entry Accounts.”

Banks usually have been criticised in current weeks for not passing on price will increase to their prospects following will increase within the Financial institution of England financial institution price, which now stands at 1.75%.

There’s hypothesis that the speed may rise to 2.25% when the Financial institution subsequent proclaims its new degree on 15 September – a rise that may heap extra stress on establishments to pay extra to savers.

5 August: Financial institution Charge Rises – However Savers Nonetheless Battle Inflation

The Financial institution of England’s current hike in interest rates from 1.25% to 1.75% will probably be welcome information to debt-free savers who’ve been battling in opposition to historically-low rates of interest for properly over a decade.

Nevertheless, with inflation at present at a 40-year excessive of 9.4% – eroding the worth of financial savings sooner than at any time up to now 4 many years – it turns into particularly essential to buy round for the most effective offers, even when financial savings suppliers go on the complete price improve.

Sarah Pennells, shopper finance specialist at Royal London mentioned: “[Savers] will probably be inspired that financial savings charges, if handed on absolutely, will see charges come out of the doldrums.

“However banks and constructing societies don’t essentially increase rates of interest on all their financial savings merchandise and will not improve them by the identical quantity, so it’s value ready a couple of weeks earlier than checking comparability web sites and best-buy tables to see if you will get a greater rate of interest.”

Kevin Brown, financial savings specialist at Scottish Pleasant, mentioned: “Anybody nonetheless in a position to save needs to be inspired to take action as charges are more likely to rise. However bear in mind that if the hole to inflation widens, returns in actual phrases will proceed to fall.”

He added: “One of the simplest ways to fight that could be to contemplate investing a few of your cash”.

Newcastle Constructing Society has already introduced it would go on the complete price improve to ‘99% of its prospects’, whereas Coventry Constructing Society has dedicated to rising its financial savings charges from 1 September.

The most recent 0.5 share level improve marks the most important single leap the BoE has carried out since 1995, and takes the Financial institution price to its highest degree in 14 years.

21 July: NS&I Boosts Charges To Ship Aggressive Supply

Nationwide Financial savings & Investments (NS&I) has elevated rates of interest throughout a swathe of merchandise to convey them into line with competitor choices.

The rate of interest paid on Direct Saver, Revenue Bonds, Direct ISA and Junior ISA, will improve from right this moment (21 July 2022).

The rate of interest paid on Assured Progress Bonds, Assured Revenue Bonds and Fastened Curiosity Financial savings Certificates will improve from 1 August 2022. These merchandise usually are not at present on sale, so the brand new charges are solely obtainable to present prospects.

Greater than 1.3 million individuals will see a lift to their financial savings on account of the will increase.

The speed on the Direct Saver and Revenue Bonds merchandise will greater than double from 0.50% to 1.20%, the Direct ISA from 0.35% to 0.90%, and the Junior ISA from 1.50% to 2.20%.

Extra substantial will increase are happening on assured and stuck curiosity merchandise. For instance, three-year Assured Revenue Bonds are rising from 0.36% to 2.50%.

Particulars of the modifications can be found here.

Earlier this yr NS&I elevated the Premium Bonds prize fund, which improved the percentages of profitable from 34,500 to 1 to 24,500 to 1 and noticed an extra 1.4 million prizes paid out in June.

11 July: Price-Of-Dwelling Disaster Bites Into Savers’ Lockdown Good points

Monetary features made by UK savers throughout lockdowns imposed on them by the Covid-19 pandemic have been slashed again on account of the continuing cost-of-living crisis and wish to fulfill rising prices, in accordance with wealth supervisor Quilter.

Analysis carried out on behalf of the corporate discovered that simply over half (53%) of the nation put aside cash in financial savings and investments in the course of the spate of coronavirus lockdowns that had been imposed on the nation throughout 2020 and 2021.

Quilter mentioned that child boomers – these born between 1946 and 1964 – had been probably to have saved cash throughout pandemic-enforced lockdowns. Of this cohort, properly over half (59%) mentioned they had been but to dip into these funds.

In distinction, the wealth supervisor discovered that round one-in-seven (15%) of those that had saved cash throughout lockdowns had already spent the money they’d put to at least one facet.

As well as, greater than a 3rd of individuals (39%) advised Quilter that they’d already made a major dent of their financial savings, with many spending as much as three-quarters of the cash they’d squirreled away.

Quilter added that just about half (46%) of Brits with lockdown financial savings had wanted to dip into their cash within the second quarter of this yr. This was a major improve in contrast with the primary three months of 2022, thanks primarily to rising meals prices adopted carefully by hovering gasoline costs.

Ian Browne, monetary planning knowledgeable at Quilter mentioned: “Whereas many individuals had been in a position to save in the course of the lockdowns and have had these funds to fall again on in the course of the cost-of-living disaster, virtually half had been unable to avoid wasting within the first place and could possibly be left in a financially weak place.”

“Even those that had been in a position to put some cash apart have seen their financial savings quickly swallowed up by rising prices, significantly on day-to-day payments resembling meals, automobile gasoline and heating and electrical energy.”

16 June: Take Benefit Of Financial institution Charge Hike, Savers Informed

Monetary specialists have urged savers to make the most of today’s decision by the Bank of England (BoE) to lift the Financial institution Charge by 1 / 4 of a share level.

As anticipated, the BoE hiked rates of interest from 1% to 1.25% which implies dangerous information for mortgage prospects on variable price offers, however provides a glimmer of hope to savers trying to make most use of their cash held on deposit.

With the newest information exhibiting that shopper costs rose by 9% within the yr to April, discovering the highest-possible price is important for savers in the event that they need to partly offset excessive inflation ranges.

Alice Haine, private finance analyst on the funding platform Bestinvest, mentioned: “For money savers, an rate of interest rise is at all times a superb factor, as they will safe greater charges on their financial savings pots – that’s after all if they’ve spare money to avoid wasting within the first place.

“Saving charges have been creeping as much as the best ranges seen in a decade, with some accounts now providing as much as 1.56% for simple entry accounts and as much as 3% for fixed-rate merchandise.

“Each penny in extra curiosity is a bonus when excessive inflation is consuming away on the buying energy of incomes. With many households dipping into emergency pots to fulfill rising meals, gasoline and power payments, it is advisable be certain that your cash is working as arduous as it might.”

Myron Jobson, senior private finance analyst at interactive investor, mentioned: “Greater charges imply financial savings will earn extra – though some banks and constructing societies have been fiendishly gradual in passing on current hikes to the bottom price.

“With the speed of inflation now greater than the most effective financial savings deal available in the market, any cash in financial savings loses buying energy over time – however it nonetheless pays to select probably the most aggressive account.”

Les Cameron, monetary knowledgeable at M&G Wealth, mentioned: “Whereas right this moment’s announcement isn’t any shock, what stays to be seen is whether or not this rise will translate to greater charges obtainable to savers or to elevated borrowing prices.

“Reviewing your funds to be sure you’re ready for the long run has by no means been extra essential and, for a lot of, that may contain searching for some type of skilled monetary recommendation.”

15 June: UK Savers Rely On Financial savings In Summer time

UK shoppers usually tend to dip into their financial savings in August than in every other month of the yr, in accordance with Atom Financial institution.

The analysis, which analysed buyer financial savings habits between Could 2020 and April 2022, additionally discovered that the first is the preferred day of every month to make a financial savings withdrawal.

Since happening vacation was the ‘prime financial savings aim’ amongst Atom prospects, it’s seemingly that many August financial savings withdrawals are being put in direction of topping up journey bills.

Aileen Robertson, head of financial savings on the financial institution, mentioned: “A standard mistake individuals make when saving for a vacation isn’t accounting for sufficient spending cash, which can lead to surprising extra bills whilst you’re away.

“It’s helpful to plan forward — analysis which excursions you may need to take and the way a lot on common they price, think about transport prices for the entire journey and contemplate what you’re more likely to spend on food and drinks.”

Nevertheless, within the midst of the continuing cost-of-living crisis, many others are more likely to be utilizing financial savings to make ends meet.

Ms Robertson mentioned: “Many individuals with good intentions to avoid wasting are seemingly feeling worse off proper now, and tapping into financial savings could also be seen as the one option to beat the present price of dwelling squeeze.”

The financial institution additionally discovered that savers tended to withdraw comparatively small quantities, with 25% of consumers taking out £80 or much less.

8 June: 50,000 Lifetime ISA Holders Use Funds To Purchase First Residence

Gross sales of stocks and shares individual savings accounts (ISAs) surged in the course of the pandemic, in stark distinction to cash ISAs, which noticed their recognition plummet over the identical interval, in accordance with the newest figures from HM Income & Customs (HMRC).

ISAs are tax-efficient wrappers that allow holders to shelter a sure amount of cash annually – at present £20,000 – from revenue tax, dividend tax and capital features tax.

HMRC says buyers opened almost 3.6 million shares and shares ISAs in the course of the 2020/21 tax yr, a interval that coincided with probably the most disruptive interval of the Covid-19 pandemic.

This is a rise of round 860,000 accounts in contrast with the earlier tax yr, representing an additional £10 billion in investments year-on-year.

HMRC says the variety of money ISAs opened throughout 2020/21 fell by 1.6 million to only over 8 million. This meant that the share of money ISAs as a proportion of the general variety of ISAs bought fell from 75% within the tax yr 2019/20 to 66% in 2020/21.

General, round 12 million ISAs had been taken out in the course of the tax yr 2020/21 equating to round £72 billion in money phrases. This compares with the 13 million accounts taken out within the earlier tax yr.

HMRC figures additionally reveal that fifty,800 individuals made withdrawals from their Lifetime ISA (LISA) to purchase a house in 2020/21, a rise of 15,000 on the earlier tax yr.

LISAs permit individuals over 18 and below 40 to avoid wasting, tax-free, for his or her first house or to complement their retirement earnings. HMRC says that the common LISA withdrawal was £13,192 in 2020/21, a £700 improve on the earlier yr.

Bestinvest’s Adrian Lowery says the figures present how households channelled lockdown financial savings in direction of investing: “In the course of the pandemic financial savings growth many households seemed in direction of investments, slightly than money financial savings, with the Financial institution of England having slashed rates of interest to an all-time low of 0.10% in March 2020.”

24 Could: NS&I Provides £40 Million To Premium Bonds Prize Fund

Nationwide Financial savings and Funding (NS&I), the Authorities-backed financial institution chargeable for Premium Bonds, has introduced a rise to its prize fund price from 1.00% to 1.40%, with impact from subsequent month.

It should imply an extra 1.4 million prizes will probably be issued in June’s month-to-month draw out of an elevated prize pot value £40 million.

The vast majority of these further prizes will probably be valued at £25 or £50, however the variety of greater worth prizes can be rising. For instance, there will probably be 98 prizes of £10,000 in every month-to-month draw from June, in contrast with the present 58, and 40 prizes of £25,000 in comparison with the present 24.

The chances of every £1 Premium Bond quantity profitable a Premium Bonds prize will even change from 34,500 to 1 to 24,500 to 1.

Ian Ackerley, chief government of NS&I mentioned: “The brand new prize fund price ensures that Premium Bonds are priced appropriately when in comparison with the rates of interest supplied by our rivals.

“It additionally ensures that we proceed to steadiness the pursuits of savers, taxpayers and the broader monetary companies sector.

Premium Bonds, that are held by over 21 million individuals within the UK, had been first launched in 1956 as a substitute option to make investments cash. Slightly than incomes curiosity each month like common financial savings accounts, buying a Premium Bond means being entered right into a month-to-month prize draw for money sums.

These sums vary in worth from £25 to £1 million, which winners obtain tax-free. Each £1 invested in Premium Bonds is equal to at least one entry into the prize draw, however the minimal funding degree is £25. Savers can money out a portion or all of their bonds at any time.

Though buyers don’t earn month-to-month curiosity, the entire worth of the prize fund will increase at a set price, which is sometimes adjusted consistent with inflation and interest rates, each of which have been climbing.

11 Could: Extra Than Half Of UK Adults Open Financial institution Accounts With out Checking Curiosity Charges

Greater than half (52%) of adults within the UK have opened a checking account with out checking the speed of curiosity it pays, in accordance with a survey by the financial savings platform, Raisin.

Little curiosity in charges

It discovered that whereas virtually half of all adults should not have a financial savings account, of those that do, greater than a 3rd have by no means checked rates of interest elsewhere to see in the event that they could possibly be getting a greater deal.

The survey, which requested 2,000 adults about their banking habits, revealed that ease of entry to their money was extra essential to savers than rates of interest.

Of the respondents with a present account, financial savings account, or ISA, simply 25% mentioned they opened it due to the rate of interest.

By comparability, 37% opened their account as a result of it was supplied by their present supplier by on-line banking. And with 23% of girls and 25% of males utilizing on-line banking every day in accordance with the survey, financial savings provides are seen by a major variety of prospects.

Department versus digital banking

Regardless of the recognition of on-line banking, Raisin’s survey discovered conventional banks and constructing societies — with bodily branches — stay extra common than their digital counterparts.

Nationwide was the preferred, with 57% of consumers responding that they favored the supplier. It was adopted by Halifax which was favored by 51% of consumers.

The Raisin survey additionally revealed that, as soon as UK savers have selected a financial institution, they recurrently keep it up for years. Greater than a 3rd (35%) of respondents mentioned they’ve the identical checking account they opened with their mother and father as a toddler. Individuals aged below 35 and below are even much less more likely to have modified banks, with 50% of them retaining the account opened with their mother and father.

Since banks and constructing societies usually entice new prospects with excessive preliminary rates of interest and even money bonuses, sticking with the identical financial institution for years is unlikely to internet you the most effective deal.

With the UK within the grips of file inflation and the cost-of-living crisis, discovering probably the most aggressive financial savings accounts is especially urgent.

Commenting on the analysis Kevin Mountford, Raisin’s co-founder, mentioned: “The market is extremely aggressive due to on-line and challenger banks vying in your cash, [so] do your analysis to seek out the most effective offers and charges — making smarter strikes along with your cash now may make it easier to save much more in the long term.”

29 April: Coventry BS Launches Fastened Charge ISA Vary

Coventry Constructing Society has right this moment launched 4 fastened price ISAs. The UK’s second largest constructing society is providing:

- ISA paying 1.50% till 30 September 2023

- ISA paying 1.75% till 20 September 2024

- ISA paying 1.85% till 30 September 2025

- ISA paying 2.00% till 30 September 2026

The 4 new merchandise be part of Coventry’s present Youngsters’s, Further Allowance, and Straightforward Entry ISAs.

Tom Riley, director of banking and financial savings at Nationwide Constructing Society, mentioned: “Many individuals will probably be looking for the most effective charges they will discover, suiting their particular person saving wants with the peace of thoughts {that a} fastened price offers, so we anticipate these new ISA merchandise will probably be highly regarded.

“ISAs are nonetheless a lovely choice for these savers desirous to earn curiosity tax-free that doesn’t depend in direction of their private financial savings allowances.”

The Coventry charges arise properly in opposition to different suppliers, together with Aldermore, which provides a one yr fastened price ISA paying 1.46% AER, and Skipton Constructing Society, which provides 2.00% AER on its three yr On-line Fastened Charge Money ISA.

Nationwide Constructing Society can be rising a few of its ISA rates of interest, together with its Single Entry ISA, by as much as 0.25% from 1 Could 2022.

14 April: Mistaken Savers Assume Inflation Leaves Them Higher Off

Almost one-in-nine (13%) money ISA savers consider that inflation will depart them higher off, in accordance with analysis from Authorized & Basic (L&G). Greater than half (52%) have no idea what affect inflation can have on the true worth of their financial savings over time.

ISA stands for ‘individual savings account’, a tax-efficient monetary product supported by the UK authorities.

UK inflation climbed to 7% earlier this week, its highest degree for 30 years. Inflation has risen sharply in current months resulting from quite a lot of causes, together with, the worldwide financial system waking up after the pandemic, a spike in world power costs and the Russian invasion of Ukraine.

Regardless of this, and with inflation predicted to soar even greater later this yr, L&G’s analysis prompt that a lot of Britons could possibly be in for a monetary shock.

L&G mentioned that there was £136 billion sitting in money ISA accounts paying a median rate of interest of 0.26%. However it added that two-thirds (64%) of money ISA savers have taken no motion on their financial savings, though the return on money was being far outstripped by the speed of inflation.

The corporate calculated {that a} £1,000 deposit with an rate of interest of 0.26% would successfully cut back in worth by £243 over 5 years assuming inflation stayed at 6% over that interval.

Emma Byron, managing director at L&G Retirement Options, mentioned: “Inflation is at its highest price for 3 many years and it’s worrying that savers don’t realise that it’s consuming away at thousands and thousands of kilos sitting in low-interest paying accounts. Understanding the affect of inflation is essential to know how a lot cash you could have in actual phrases.

“Whereas it’s important to maintain some money within the financial institution for an emergency fund, savers may need to contemplate different choices to make their cash work more durable.”

29 March: JP Morgan’s Chase Gives 1.5% Financial savings Account

Chase, JP Morgan’s new digital financial institution, has unveiled a financial savings account for UK prospects paying curiosity at twice the extent of the Financial institution of England (BoE) Financial institution price.

The Chase saver account is linked to the supplier’s personal present account and provides a aggressive rate of interest of 1.5% AER.

AER, or Annual Equal Charge, is the official technique of calculating and exhibiting the rate of interest for financial savings accounts and is designed to permit straightforward comparisons throughout related merchandise.

Earlier this month, in a bid to stave off steepling UK inflation, the BoE raised its Financial institution price from 0.5% to 0.75%, the third rise in 4 months.

The JP Morgan saver account is offered to new and present Chase present account holders and might be opened through the corporate’s app.

Chase mentioned savers can deposit as much as £250,000 in whole at any time and may entry their financial savings every time they need, penalty-free and with out lack of curiosity. There is no such thing as a minimal opening steadiness.

Analysis from Chase discovered that UK shoppers are in search of methods to section their money so as to higher save for particular targets. Clients can open a number of Chase saver accounts to realize this, every with a personalised identify and that includes a novel account quantity.

The UK’s private financial savings allowance (PSA), launched in 2016, permits basic-rate (20%) taxpayers to earn £1,000 in financial savings curiosity tax-free, whereas higher-rate (40%) taxpayers are allowed to earn as much as £500 earlier than tax. Further-rate (45%) payers obtain no allowance.

A basic-rate taxpayer would be capable of deposit slightly below £70,000 within the new Chase saver account with none tax legal responsibility on the product’s current price. A better-rate taxpayer may have round £34,000 on deposit with the account and never bust the £500 tax-free curiosity restrict.

Shaun Port, Chase’s UK managing director for financial savings and investments, mentioned: “With the price of dwelling rising, we all know that buyers need to maximise the curiosity they will earn with the reassurance of with the ability to entry their financial savings immediately. We’ve designed the Chase saver account to supply our prospects with most flexibility alongside a aggressive price.”

The UK’s Financial Services Compensation Scheme is a monetary lifeboat association that protects prospects holding as much as £85,000 throughout all accounts held throughout the umbrella of 1 banking group.

24 March: Monument Launches Trio Of Financial savings Accounts

New digital financial institution Monument has launched a trio of fixed-term financial savings merchandise which, it claims, pay aggressive charges of curiosity.

Accessible through its app, Monument’s 12-month, fixed-term financial savings account pays an annual equal price (AER) of 1.80%. AER is the official price for financial savings accounts and is designed to permit straightforward comparisons throughout related merchandise.

A two-year model of the account pays 2.05% AER, whereas Monument’s five-year, fixed-term product options an AER of two.40%.

Depositors should be 18 over and resident within the UK. Clients are required to carry a minimal steadiness of £25,000 at any time throughout Monument financial savings accounts to qualify for the revealed charges.

Ought to they modify their thoughts, prospects can cancel an account inside 14 days of opening one. As soon as up and working, nevertheless, withdrawals usually are not permitted.

Monument, which describes itself because the “first neo-bank launched within the UK particularly to fulfill the unmet calls for of mass prosperous purchasers”, acquired its banking licence final yr.

John Saunders, Monument’s chief industrial officer mentioned: “We’re happy to offer a spread of financial savings selections to contemplate, all at aggressive charges. Inflation is an actual and rising characteristic of private finance, so leaving financial savings in low, or no, interest-bearing accounts makes much less sense than ever.”

1 March: Examine reveals regional variations in UK saving habits

One in 4 individuals within the UK should not have sufficient money for emergencies, in accordance with funding platform Hargreaves Lansdown (HL).

The agency defines emergency money as financial savings equal to no less than three months’ value of important bills.

Figures from its Financial savings & Resilience Barometer, a monetary measure put along with consultants Oxford Economics, confirmed a large regional disparity in UK financial savings habits in the beginning of 2022.

HL recognized the North of England, Midlands, Devon and Wales as amongst 10 so-called ‘notspots’, or areas that featured giant shortfalls for money financial savings.

In keeping with HL, greater than a 3rd (36%) of these within the West Midlands and Tees Valley and Durham reported that they don’t have sufficient money put aside in financial savings.

The identical state of affairs was additionally reported by a 3rd of individuals (33%) in Northumberland, Tyne and Put on, Derbyshire, Nottinghamshire, Devon and West Wales.

This contrasted with elements of London and the Residence Counties, together with Hertfordshire and Bedfordshire, that HL dubbed as financial savings ‘hotspots’, the place greater than 4 in 5 individuals claimed they’ve enough quantities of emergency money.

HL’s Sarah Coles mentioned: “There’s a mountain to climb to degree up monetary resilience throughout the UK. The report reveals a gulf between areas with loads of financial savings and people with large shortfalls. It’s not merely a North/South divide.”

Individually, monetary teaching app Claro Cash says greater than 1 / 4 (28%) of Brits are counting on nest-eggs to make good shortfalls when outgoings exceed their revenue, slightly than utilizing their financial savings for aspirational targets resembling shopping for a automobile or taking a luxurious vacation.

Sarah Brill at Claro Cash mentioned: “Financial savings are being known as upon to fulfill the every day price of dwelling with inflation will increase at a 30-year excessive. Beforehand, spending habits might need seen Brits save to spend on rewarding massive ticket gadgets, however it’s now the mounting price of dwelling that’s nibbling away at Brits’ hard-earned financial savings.”

15 February: NS&I Doubles Inexperienced Financial savings Bond Charge

Authorities-backed Nationwide Financial savings & Investments has issued a second tranche of its inexperienced financial savings bond paying 1.3% over a three-year fastened time period – twice the quantity paid on the primary situation of the bond at launch final October.

Somebody shopping for £1,000 of the brand new bonds, which allow savers to place their cash behind initiatives resembling renewable power and cleaner transport, will obtain £1,039 at maturity.

Main three-year bonds on supply from monetary establishments are paying round 1.8%.

The most recent situation has a minimal preliminary deposit of £100 and the utmost funding is £100,000 per particular person. As NS&I is backed by the UK Treasury, 100% of savers’ cash is protected. Candidates must be no less than 16.

Financial savings with different suppliers are protected as much as £85,000 per particular person below the Financial Services Compensation Scheme.

As soon as an preliminary deposit has been made, a 30-day cooling off interval offers savers the chance to withdraw their money. After that, savers are prevented from accessing their cash till the bond reaches the top of its time period.

Sarah Coles at Hargreaves Lansdown says NS&I’s resolution to double the inexperienced bond’s rate of interest is “a dramatic step that reveals the previous price was an actual disappointment”.

She says the upper price “could also be sufficient to see the bond flourish”.

Becky O’Connor at on-line platform interactive investor, says: “Whereas this price isn’t prime of the best-buys for three-year bonds, that are at present round 1.8%, it’s much more compelling than earlier than for these wanting their cash to be put to productive use within the UK’s rising low carbon financial system, at no danger.”

10 February: NS&I Ups Charges On Direct Saver And Revenue Bond Accounts

NS&I, the government-backed financial savings supplier, is elevating the rates of interest on its Direct Saver and Revenue Bond merchandise to 0.5% gross Annual Equal Charge (AER) from right this moment (10 February).

The rise in every case of 0.15 share factors follows an increase from 0.15% to 0.35% final December. Final week, the Financial institution of England raised its official Financial institution price to 0.5%, its second improve in three months.

The Direct Saver account might be opened with a minimal deposit of £1 with an higher restrict of £2 million, whereas the Revenue Bond has a minimal funding of £500 and a most of £1 million.

Ian Ackerley, NS&I chief government, mentioned: “The brand new rates of interest will guarantee our merchandise are priced consistent with the broader financial savings sector.”

Helen Morrissey at monetary advisor Hargreaves Lansdown mentioned: “It’s massively optimistic to see NS&I boosting charges on these merchandise, however they nonetheless stay a way off assembly the most effective charges obtainable available on the market.

“The most effective easy-access financial savings price obtainable is at present 0.71%, so savvy savers keen to buy round can nonetheless discover higher locations to stash their money.”

8 February: Straightforward-Entry Merchandise Dominate 2021 Financial savings Market

UK savers selected to squirrel away their cash in easy-access accounts final yr over fixed-rate merchandise or Particular person Financial savings Accounts (ISAs), in accordance with Aldermore Financial institution.

Evaluation by Aldermore of the newest Financial institution of England Money and Credit information confirmed that UK private financial savings stood at £1.414 trillion in December 2021, a year-on-year improve of 6.5%, or £86 billion.

Aldermore attributed the rise to a continuation of the financial savings habits that Brits picked up in the course of the 2020 lockdown when the pandemic was at its top. The determine excludes money held in present accounts and NS&I merchandise resembling Premium Bonds.

The financial institution mentioned the easy-access ingredient of the financial savings market attracted an extra £99 billion in 2021, a rise of 11.3% year-on-year. The primary benefit of easy-access accounts is that they permit savers to withdraw money as and once they please.

In distinction, Aldermore mentioned that the quantity in fixed-rate financial savings merchandise on the finish of 2021 was £9 billion down on the earlier yr, a drop of 5.7%.

The analysis additionally confirmed that savers deposited £4 billion much less in savings-based ISAs by the top of final yr in contrast with 12 months earlier, with the attraction of tax-free advantages from these merchandise failing to offset the depressed rates of interest on supply.

Ewan Edwards, financial savings director at Aldermore Financial institution, mentioned: “The worth of financial savings can’t be underestimated. It’s very encouraging that the concentrate on financial savings we noticed in 2020 has continued on and grown additional in 2021 as individuals stay centered on constructing their monetary wealth.”

Common Financial savings On The Rise

Separate analysis from Paragon Financial institution backed up the pattern in direction of higher financial savings habits. In keeping with the financial institution, the common non-ISA easy-access steadiness grew from £10,246 in March 2020 to £12,106 in October 2021.

However Paragon warned that almost all of those accounts proceed to earn a really low rate of interest, with 71% of easy-access balances providing an rate of interest of 0.1% or much less.

The financial institution added that the variety of easy-access, non-ISA accounts with balances of £100,000 or extra now makes up a file 2% of all accounts on this sector. That is up from 1.8% in October 2020 and 1.6% in October 2019.

Derek Sprawling, financial savings director at Paragon Financial institution, mentioned: “The dominant pattern we’re noting within the easy-access house is that seven out of 10 savers proceed to obtain a extremely low return on their cash.

“That is regardless of charges choosing up throughout the board and best-buy offers providing individuals the chance to earn no less than six instances extra curiosity than they at present are in a low-paying account.”

from Lifetime Savings SP – My Blog https://ift.tt/Opz4qtZ

via IFTTT